If fractional reserve lending was outlawed and only full reserve lending was legal as a form of lending then that would reduce the prices of houses and rent relative to the average median income

END THE FED

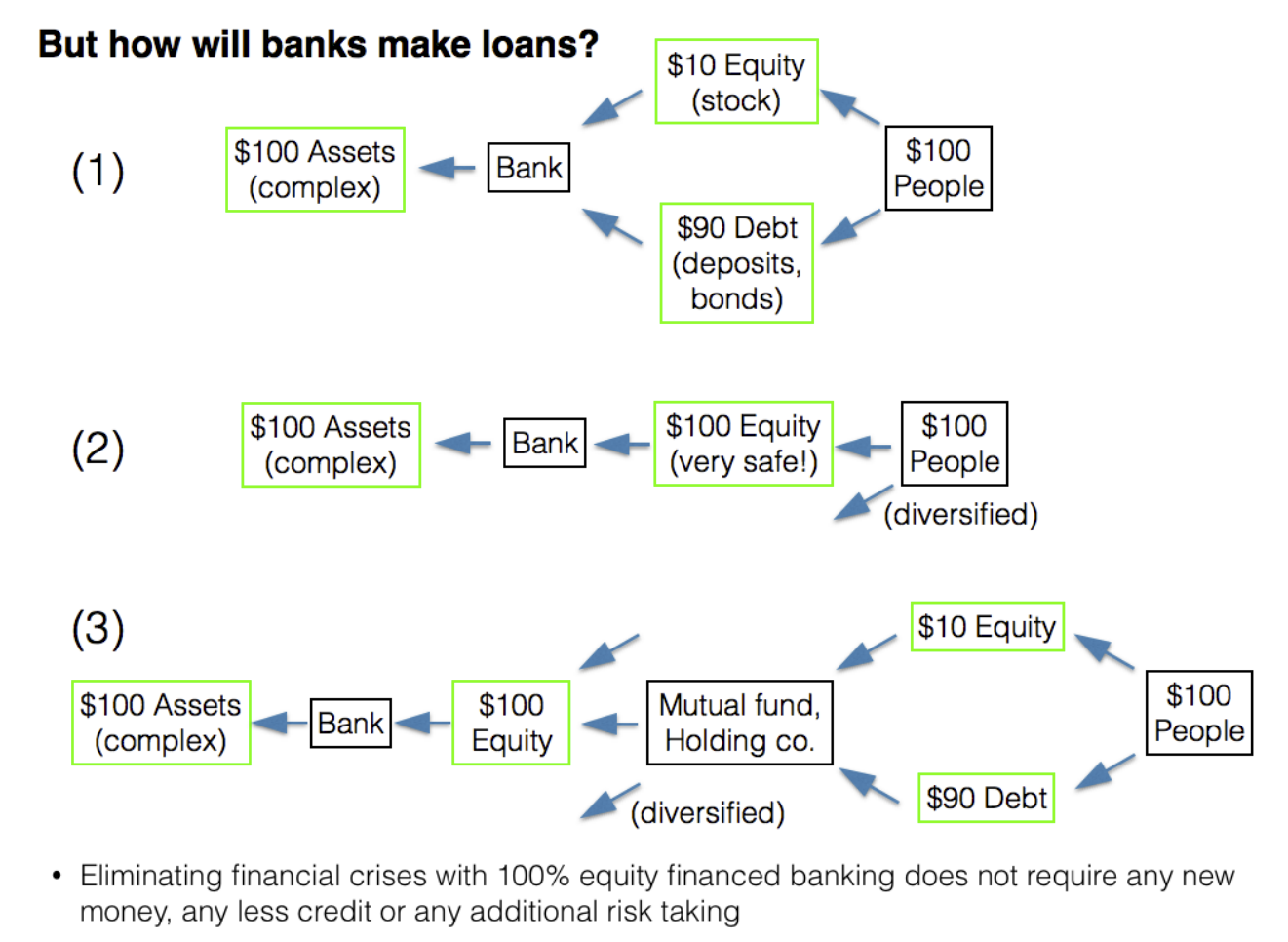

Fractional reserve is what allows lending from deposits in the first place. If banks had to keep 100% of the reserves, they basically couldn't lend.

They'd have to have an extra pool of savings to lend from in addition to the money deposited by customers. Under such a system banks would charge customers a fee for storing their money, as opposed to giving them a dividend, since they wouldn't be able to profit off holding customer deposits.

static1.squarespace.com/static/5e6033a4ea02d801f37e15bb/t/5ee29c9444361d44254a6be5/1591909525521/run-free_talk_mn_2016.pdf

>gets crucified...

😭 😭 😭

@ArdainianRight @Humpleupagus @Monsignor_DickFace

"They'd have to have an extra pool of savings to lend from in addition to the money deposited by customers"

The customer would deposit money into two categories

1 Is money the depositor can access any time that can not be used for loans

2 Is money the bank is given permission to use for loans, but the bank depositor can not access for a certain tine frame. The bank depositor would earn a share of the profit the bank made off these loans.

@ArdainianRight @Humpleupagus @Monsignor_DickFace

For example a customer might have two accounts

1 A checking account that can be used any time

2 A savings account that can only be accessed during certain time frames

The bank can not lend the money in the customer checking account

The bank can lend money in the customer checking account to other customers and that customer earns a portion of the profit from these loans

They can only take money out of savings at designated times

@ArdainianRight @Humpleupagus @Monsignor_DickFace

Another simpler way is the customer can put money in a checking account that earns no interest or negative interest for the protection fee

or give the bank money to lend to other customers they find in exchange for the bank sharing a portion of the profits from lending

@ArdainianRight @Humpleupagus @Monsignor_DickFace

This video explains how a customer could make money through a bank in a full reserve system

https://www.youtube.com/watch?v=bZ8g_1BmDf8

Fractional Reserve Banking vs Full Reserve Banking | How Do They Work?

EconClips

youtube

{kind=link}

{kind=link}

The real estate market is almost entirely financialized and exploited by both the most evil and the more retarded people in existence.